Florida’s condo landscape is in flux. After years of subtle warning signs, the market is finally beginning to reflect the pressure, with shifts in pricing, regulation, and buyer behavior that are reshaping how condos are valued and sold across the state.

Whether you own a condo or are considering buying one, understanding what’s driving these changes can help you make more informed decisions moving forward.

Let’s dive into what’s happening and why it matters.

What the Data Is Showing

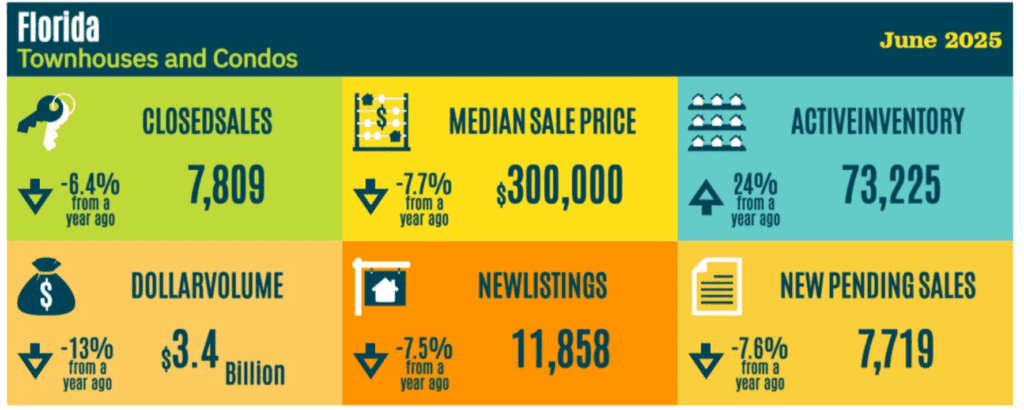

According to SunStats, the median price for condos and townhomes in Florida was $300,000 as of June 2025, about 8% lower than the same time last year. While that may not sound dramatic at first glance, some areas have seen much sharper adjustments.

For example:

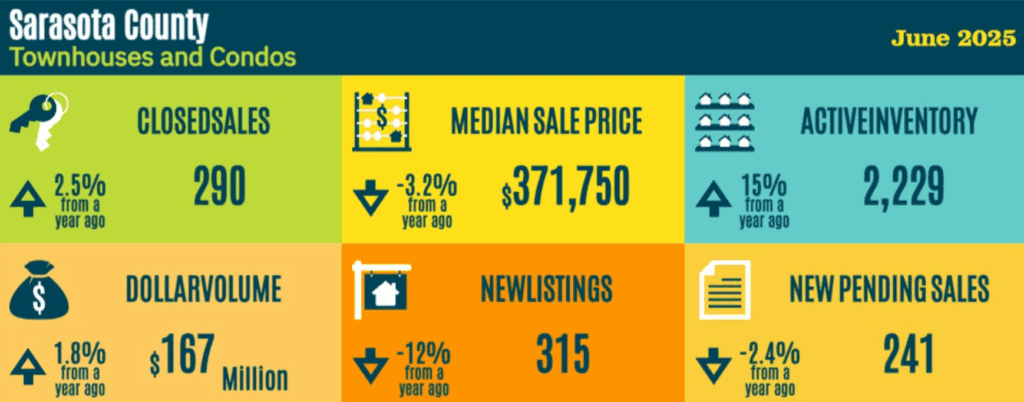

- In Sarasota County, the median price fell 13% year-over-year to $321,000 in May, with nine months of inventory on the market. In June, the median price was $371,000, -3% vs STLY, perhaps indicating that the condo market is leveling in Sarasota County.

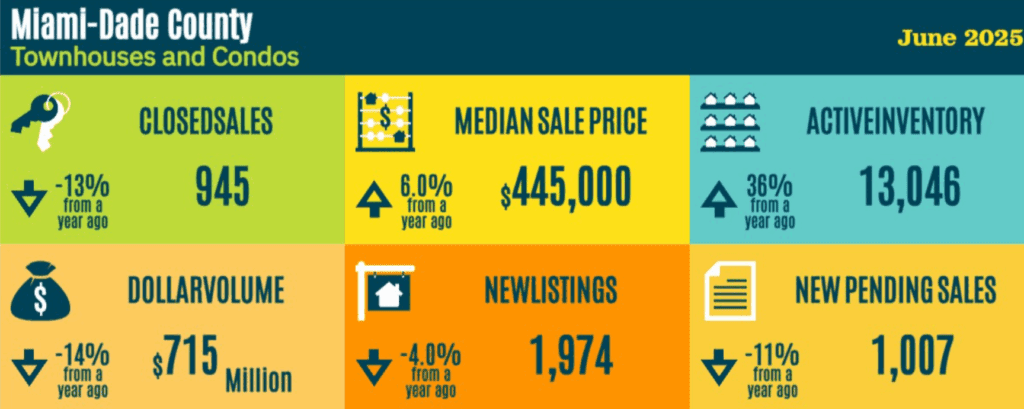

- Miami-Dade shows a median price of $445,000, up by 6% from the same time last year, but that’s largely influenced by new luxury construction. Behind the scenes, older buildings are experiencing longer market days and growing inventory (+36%).

Other regions in Florida have seen a drop of over 20-30% vs the same time last year. Across the board, listings are up significantly, with nearly 80,000 condos and townhomes for sale statewide in May, a 30% increase from the previous year. That’s a signal that more owners are choosing to list, even in a changing environment.

What’s Fueling the Shift?

A big part of the story stems from the tragic Surfside building collapse in 2021, which prompted significant changes to state law.

Florida now requires:

- Milestone structural inspections for older buildings (30+ years, or 25 years near the coast)

- Structural reserve studies (SIRS) to assess long-term repair needs

- Mandatory reserve funding, associations can no longer waive contributions

These changes aim to improve safety and transparency, which is a positive step for the long-term health of the building. However, they’ve also presented financial and logistical challenges for some communities, especially those that are underfunded or have not yet completed their inspections.

For prospective buyers, these new requirements create more due diligence. For current owners, these introductions present important and sometimes urgent planning decisions.

Rising Costs and Insurance Complications

Florida’s well-documented property insurance crisis continues to put pressure on condo buildings. In some cases, master insurance policies have more than doubled, or even tripled, in cost. These increases can result in higher monthly fees or special assessments when budgets are insufficient.

Some associations have passed assessments ranging from $20,000 to $100,000 per unit. That’s not the norm everywhere, but in certain buildings, it’s becoming more common.

There are also financing challenges. Some buildings now appear on Fannie Mae’s “unavailable” list, which means buyers can’t secure conventional mortgages there. While this doesn’t make a sale impossible, it can narrow the buyer pool and influence pricing. The list isn’t public, but lenders can access it, and it’s worth checking if your building may be affected.

New Legislation Offers Breathing Room

As of July 1, 2025, House Bill 913 is in effect, giving associations more time and flexibility to meet inspection and reserve requirements.

Key highlights:

- Extended deadlines through the end of 2025

- A two-year pause in reserve contributions after inspections are completed

- Permission for associations to secure loans or lines of credit to help fund reserves, something that wasn’t allowed before (note that condo owners need to agree to this)

These changes are designed to ease the transition and provide practical options for communities with tighter budgets, including many with older residents.

What Happens Next?

Market conditions are expected to remain mixed throughout the remainder of 2025. Some areas may continue to experience price adjustments as inventory increases and buyers become more discerning. But buildings that are well-maintained, transparent with their documentation, and financially stable are holding up better, and in some cases, stand out in the crowd.

By late 2026, the market is expected to begin stabilizing (this is the current projection, which may evolve). Buyers will have more clarity, and buildings that have completed their inspections and funding plans will likely be more in demand. The difference between compliant and non-compliant buildings is already becoming more pronounced, and that trend is expected to continue.

Final Thoughts

Florida’s condo market is in crisis, but it is starting to level out. The landscape is becoming more complex, and the gap is widening between well-managed buildings and those struggling to adapt.

Whether you’re buying, selling, or just holding, now’s the time to stay informed. The rules have changed, and so have the expectations.

Do you have questions about how your building fits into this picture? Curious, what’s happening in your local area? I’m always happy to discuss the data and help you make sense of it – no pressure, just perspective.

Katrin Pfitzenreiter

Broker Associate | Real Estate Market Analyst

Coldwell Banker Realty

Sources:

https://www.newsweek.com/condo-prices-see-second-largest-drop-record-2094021

https://www.redfin.com/news/condo-prices-may-2025

https://economics.td.com/us-florida-condo-market

https://www.miamiherald.com/news/business/real-estate-news/article305744786.html#newshunter

https://www.miamiherald.com/news/local/article303192396.html

https://www.newsweek.com/number-florida-condos-mortgage-blacklist-growing-2059410

https://www.propfusion.com/law-guide/florida-sirs-requirements?

https://www.nbcmiami.com/responds/rising-insurance-costs-impacting-condo-affordability/3403424

https://mosheslaw.com/why-did-condo-insurance-go-up-in-2025-a-deep-dive-into-rising-costs

Disclaimer:

The opinions shared here are my own and are intended for informational and educational purposes only. This content should not be taken as legal, financial, or professional advice. While I strive to ensure accuracy and provide useful insights, I can’t guarantee the completeness or reliability of the information presented.

I encourage readers to do their own research and consult with qualified professionals before making any real estate, financial, or legal decisions.

Any discussions of real estate trends, policy changes, or market commentary reflect my personal views and are based on publicly available data and credible sources that I believe to be accurate at the time of writing. I am not liable for any decisions or actions taken based on the content of this post.